Rates Are Dropping—So Is Everyone’s Jaw (Kind Of): What the Fed’s Move Means for Manhattan Real Estate

By Kelly Robinson

August 2025

After over a year of mortgage rates playing hard to get, the Fed is finally putting some skin back in the game. Rate cuts are back on the table, inflation is cooling, and suddenly everyone from first-time buyers to brownstone collectors wants to know: is this the moment?

Sort of. But before we all start refinancing our dreams, let’s unpack what’s actually happening, and what it means for Manhattan real estate.

First: What Just Happened?

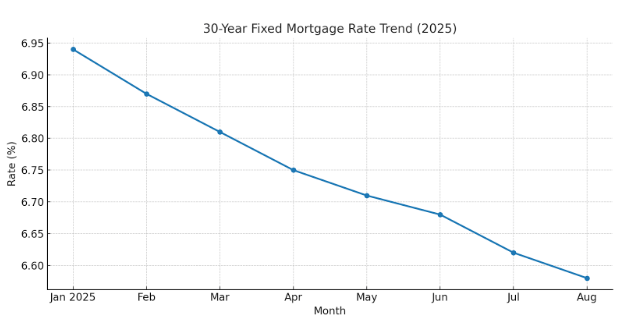

The Federal Reserve hasn’t pulled the trigger just yet, but markets are betting big on a rate cut this September. That would be the first cut since the tightening frenzy started in 2022. Wall Street is already pricing in two or three cuts by the end of the year.

But here’s the reality check: Fed rates are not the same thing as mortgage rates. They influence them, yes, but like a GPS from 2011, they’re just a suggestion.

Mortgage rates have started to tick down, but they’re still north of 6.5%—which feels like a deal only if you’ve completely blocked out 2023. Most forecasts expect only mild movement this year.

Will This Actually Help Buyers?

Yes, but slowly.

Lower rates mean lower borrowing costs. In theory, that unlocks more affordability. In reality, NYC is still one of the most expensive housing markets in the world. A quarter-point drop isn’t going to magically turn Tribeca into a fire sale.

What it can do:

-

Entice fence-sitters to make a move

-

Nudge up buyer confidence (and competition)

-

Light a fire under sluggish luxury inventory

Don’t expect a frenzy. Expect a slow burn.

Manhattan Is Not the Midwest

You might see headlines about “homebuilder confidence plummeting” or “inventory flooding the market.” That’s adorable.

Manhattan doesn’t play by those rules. We’re dealing with:

-

Limited supply

-

Locked-in sellers clinging to 3% rates

-

Buyers who are still digesting those $1,800-per-foot listings

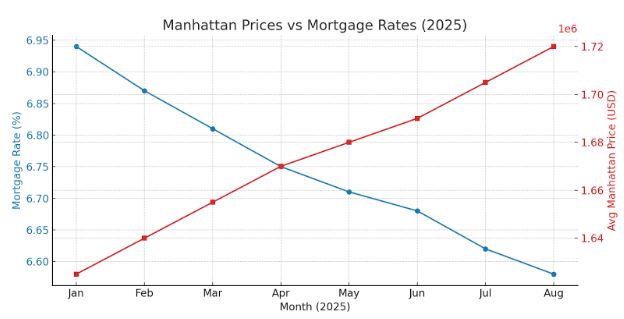

Even when rates ease, Manhattan doesn’t move fast. After the last rate drop in 2024, it took 3–4 months to see real buyer momentum in co-op and condo markets. And that was with serious pent-up demand.

What About the Luxury Market?

Luxury buyers are not hunting for deals in the Zillow bargain bin. They’re:

-

Watching currency swings

-

Monitoring geopolitical shifts

-

Buying based on lifestyle, not loan approvals

For this crowd, a dip in rates is less about monthly payments and more about timing the market narrative.

If the Fed signals confidence with rate cuts, it could boost luxury activity. Especially in neighborhoods like the Upper East Side, West Village, and those 22-foot-wide townhomes that come with a wine cave and a gym better than Equinox.

One Word: Refinancing

This could be where things get interesting.

Tens of thousands of New Yorkers have been sitting on the sidelines with renovation plans collecting dust. Why? Because borrowing at 8% for a kitchen facelift feels criminal.

A Fed rate cut could:

-

Lower HELOC rates

-

Reignite renovation projects

-

Add value to aging inventory without triggering a resale

Translation: expect to see scaffolding again, and not just the kind that stays up for no reason.

Commercial Real Estate? Still Murky

Lower rates help commercial real estate, but let’s not pretend we’re out of the woods. Office-to-resi conversions, stalled multifamily builds, and distressed assets all might catch a break. But that’s a next-year story, at best.

Developers need more than a softer Fed. They need:

-

Streamlined rezoning

-

Access to capital

-

Political will (which, let’s be honest, is always on backorder)

Bottom Line: Be Ready, Not Reactive

A rate cut is a green light, not a guarantee. If you’re buying, you’re still competing. If you’re selling, you’re still in a value-driven market. And if you’re refinancing, you’re about to get your first decent shot in years.

Just don’t expect the market to change overnight. In Manhattan, the only thing that moves fast is a G‑wagon trying to beat a red light on Park Avenue.

Want to see how this impacts your specific property or neighborhood?

Let’s talk. Because when rates start to shift, the smartest move is already being ready.