Manhattan Luxury Report | July 2025 Edition

Where the only thing hotter than a penthouse listing was the pavement.

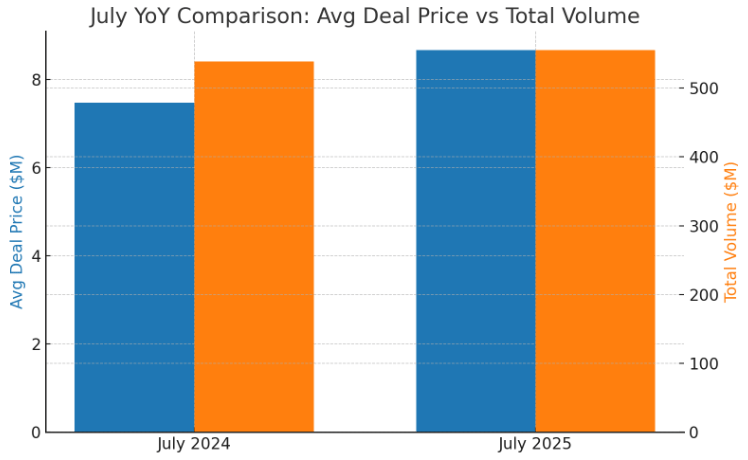

July 2025 vs. July 2024: Contracts & Prices Face Off

From June 23 to July 14:

-

2025: 64 contracts at $4M+ → Total volume ~$555.26 M, averaging about $8.67 M per deal

-

2024 (same period): 72 contracts → Total volume ~$538.65 M, averaging about $7.48 M per deal

That’s an 11% drop in deal count, but a 16% jump in average deal size. So while fewer luxury homes traded hands, buyers shelled out more per property.

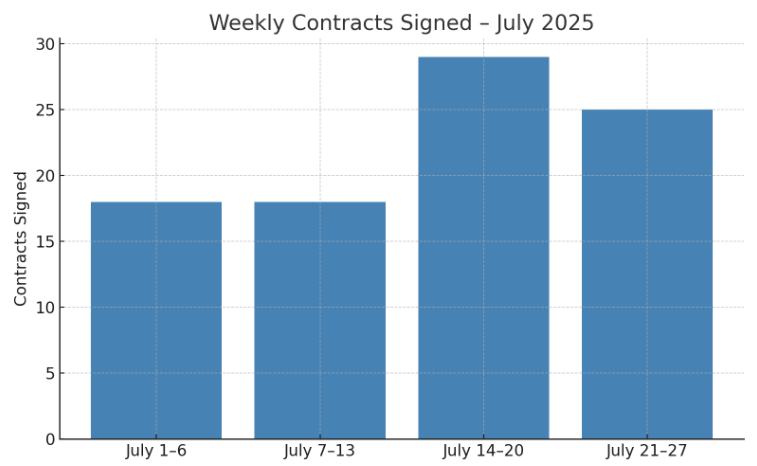

Weekly Luxury Activity: July 2025 Breakdown

|

Week |

Contracts Signed |

|

July 1–6 |

18 |

|

July 7–13 |

18 |

|

July 14–20 |

29 |

|

July 21–27 |

25 |

Mid-July (July 14–20) saw a spike to 29 contracts, despite record-breaking heat. That week’s activity was the strongest of the month—but overall, July followed the typical summer slowdown pattern.

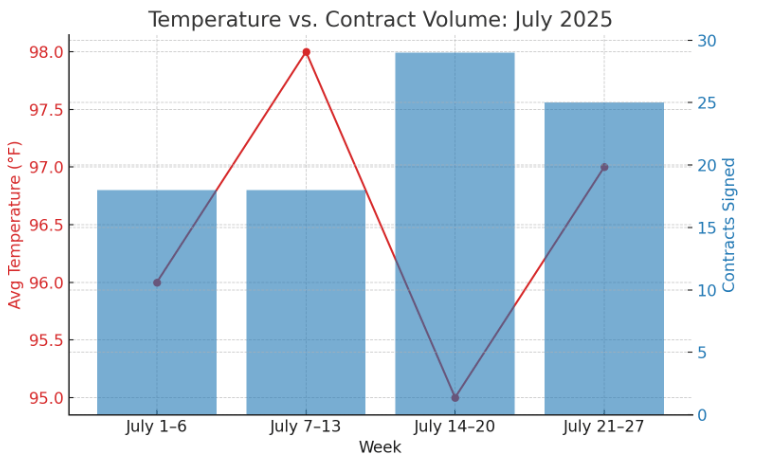

When the Heat Wave Hit, the Market Didn’t

Let’s be honest—when it’s 104°F with city steam cooking your eyebrows, even the most serious buyer would rather tour the wine fridge than a sixth-floor walkup. Showings slowed. Brokers melted. But somehow… contracts got signed.

That dual-axis chart says it all: as the mercury rose, deal counts mostly cooled—except for a brief, possibly air-conditioned resurgence in mid-July.

Price Trends Held Strong

Despite a dip in volume, closed prices remained strong. Luxury buyers may have been pickier, but they came prepared to spend—especially on turnkey or trophy-level units. Cash was king again in Q2, with 69% of luxury deals closed without financing.

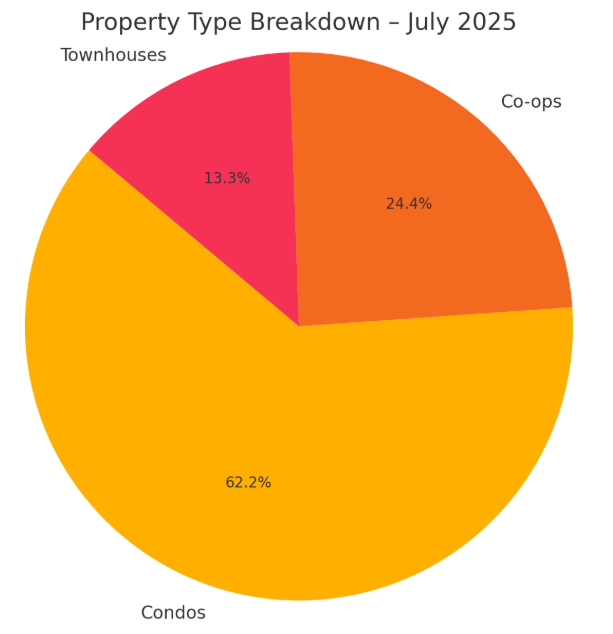

Property Type Breakdown (July 1–27)

-

Condos: Still leading the pack

-

Co-ops & Townhouses: Steady, niche-specific movement

-

Trophy Sales: Fewer, but high-dollar when they hit

The Takeaway

|

Group |

Insight |

|

Sellers |

July is slower by nature—don’t panic. Strategic pricing still wins. |

|

Buyers |

Less competition, but higher per-unit prices. Move fast, negotiate well. |

|

Investors |

Manhattan remains resilient. Deal size is up; inventory is tightening. |

Final Thought

Luxury didn’t disappear—it just got sweaty.

The buyers still circling in July are decisive and deep-pocketed. Fewer total deals? Sure. But bigger ones. And as August picks up, watch for pent-up demand to return like Manhattanites from the Hamptons.